Cryptocurrency Posts

Crypto Briefing

Coinbase's move to Abu Dhabi signals a shift towards regulated digital asset markets, potentially setting a precedent for global financial hubs.

The post Coinbase establishes tokenization hub in Abu Dhabi after FSRA approval appeared first on Crypto Briefing.

Rising optimism among US small businesses could signal potential economic resilience, but sustainability remains uncertain amid fluctuating forecasts.

The post US NFIB Business Optimism Index rises to 99.8, beating forecasts and its own historical average appeared first on Crypto Briefing.

European markets' resilience amid geopolitical tensions highlights investor optimism but remains vulnerable to potential oil price volatility.

The post European markets outperform forecasts amid Iran war concerns appeared first on Crypto Briefing.

Coinbase's UK derivatives launch could reshape institutional trading by offering a regulated, multi-asset platform, enhancing market accessibility.

The post Coinbase opens UK derivatives trading with up to 50x leverage for professional investors appeared first on Crypto Briefing.

Anthropic's IPO timing could enhance its market position, influence AI sector dynamics, and impact investor strategies amid regulatory scrutiny.

The post Anthropic targets September-October IPO ahead of OpenAI: WSJ appeared first on Crypto Briefing.

Bitcoin Magazine

Bitcoin Magazine

Blockstream Debuts Swaps, Allowing Bitcoiners to Move Between Lightning and Main Network With Ease

Bitcoin infrastructure company Blockstream has announced a new feature allowing users to make trustless swaps.

Dubbed Blockstream Swaps, the idea is that Bitcoiners will be able to quickly move between the main chain and Lightning network.

It comes after non-custodial Bitcoin swap provider Boltz suspended its service after it said attackers were finding vulnerabilities faster than its team could fix using AI.

“In support of the broader Bitcoin and Liquid ecosystem, Blockstream is launching Blockstream Swaps,” Blockstream said.

“This initiative was already under development to ensure a resilient suite of utility for the ecosystem, and it complements the providers already doing this work rather than replacing any one of them.”

The idea, added Blockstream, is users can move funds across layers while never losing full control over their funds.

To use Lightning, users will not need to run a node or channel — as is normally needed with Lightning — and can simply hold a Bitcoin or LBTC balance and let a swap convert at the moment of payment.

LBTC is the native asset of the Liquid Network, a Bitcoin layer-2 sidechain created by Blockstream.

“This initiative was already under development to ensure a resilient suite of utility for the ecosystem, and it complements the providers already doing this work rather than replacing any one of them,” added Blocksteam’s announcement.

Boltz this month suspended its Bitcoin swap service. It said that a surge in AI-assisted attacks left it unable to continue operating safely.

Crypto hacks have surged, with security experts warning that cybercriminals are using AI to search for bugs in crypto projects and then take advantage of errors auditors may have missed.

This post Blockstream Debuts Swaps, Allowing Bitcoiners to Move Between Lightning and Main Network With Ease first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

BTCPay Server Offers a 3 Bitcoin Bounty for Recovery of Stolen Funds After Wallet Exploit

Supporters of BTCPay Server have committed to funding a bounty of up to three Bitcoins for the recovery of funds stolen through a recently disclosed vulnerability in the open-source bitcoin payment processor, the project said in a statement.

The bounty is set at 10 percent of whatever is recovered, capped at three coins in the event of a full recovery.

The project even extended the offer to the attacker directly alongside anyone else holding actionable information, directing them to a dedicated security address and offering Signal or other encrypted channels on request.

Hackers last week managed to extract Lightning Network admin macaroon credentials from affected BTCPay Server instances. The project published technical details and remediation guidance in a separate security advisory.

“To the users who lost funds: we are sorry,” the project said in a statement. “We will examine our mistakes, but regret alone will not help affected users or secure the project. There is no time to waste. We have to learn, improve, and act quickly.”

The BTCPay Server Foundation said it would donate 0.21 Bitcoins to Sparrow Wallet developer Craig Raw and a further 0.21 Bitcoins to the Bitcoin Red Team fund in recognition of their responsible disclosure of the vulnerability.

Separately, the project said it has been contacted by security teams at exchanges, blockchain analytics firms and law enforcement agencies offering assistance in tracking the stolen coins.

Affected users who have not yet come forward are being asked to share on-chain addresses and transaction details, and to file reports with local authorities and any exchange or service where the funds surface.

Individual reports, the project said, help preserve records and establish a chain of evidence that improves the odds of funds being frozen.

The project added that improving AI models are making it faster and cheaper to comb large codebases for weaknesses, shifting the balance toward attackers, and that Bitcoin projects are feeling it first because they are unusually valuable targets.

This post BTCPay Server Offers a 3 Bitcoin Bounty for Recovery of Stolen Funds After Wallet Exploit first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

Bitcoin Exchange-Traded Funds See Spike In Inflows Following Huge Hack

American Bitcoin exchange-traded funds have had their biggest weekly inflow since April, taking in $850 million last week, according to Bloomberg figures.

The major U.S. funds managed by BlackRock, Fidelity, Grayscale, Morgan Stanley and others have received the cash the week after hackers targeted Coinkite’s popular Coldcard product.

Hackers started stealing millions in Bitcoin from Coldcard wallets after discovering a vulnerability in the product’s software. Some estimates put the amount of Bitcoin lost now at over $130 million.

JUST IN: BlackRock tells Bloomberg they've "seen consistently" that Bitcoin ETF investors are buying and holding BTC "long term" on this dip

— Bitcoin Magazine (@BitcoinMagazine) August 10, 2026

"That is being exhibited through this downturn." HODLpic.twitter.com/9D0j9uLJwu

The incident has rattled the BTC community that typically praises cold storage solutions.

Speaking on Bloomberg’s ETF IQ show on Monday, Robert Mitchnick, global head of digital assets at BlackRock, said that since the ETFs’ approval in 2024, investors have wanted a “very simple turnkey trusted vehicle and not have to worry about all the unique elements of Bitcoin and crypto security that generally custody otherwise would require of an investor.”

Speaking about the Coldcard hack, he added: “What’s also important to recognize is that that is not a breach of Bitcoin or any other crypto protocol — those are individual security mismanagement issues that happen from various individuals or providers.”

It isn’t clear whether investors are rotating out of cold storage into the ETFs since the hack but the funds have seen a spike in trading action.

Bitcoin’s price has typically done well when investors have thrown cash at the products but the leading cryptocurrency is now flat over a seven-day period, priced at $63,861.

BlackRock’s iShares Bitcoin Trust took most of last week’s inflows but other funds managed by Morgan Stanley and Fidelity also experienced trading action.

The U.S. Securities and Exchange Commission in 2024 approved the slew of Bitcoin investment funds which went on to have the most successful launch in the history of ETFs.

Investors previously put off from buying Bitcoin due to the complexities of cold storage and private keys can now buy shares that trade on stock exchanges that track the price of Bitcoin.

The ETFs — managed by other top Wall Street fund managers — currently manage nearly $80 billion in assets, according to Coinglass data.

This post Bitcoin Exchange-Traded Funds See Spike In Inflows Following Huge Hack first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

TD Cowen Gives Crypto Clarity Act a 25% Chance of Passing This Fall

Investment bank TD Securities has said that the long-awaited crypto Clarity Act has a slim chance of getting passed in a Monday note, citing last week’s delay and potential stalling from the Democrats.

The bank said that now the bill won’t be passed before the summer, it only has a 25% of getting passed in September.

Lawmakers were hoping a crucial vote on the long-awaited crypto market structure bill was to go ahead before a five-week recess but news dropped last week that there was a delay and now the Senate will vote on the bill in September.

“The bill is not dead, but the path forward is harder,” the bank said. “We assign a 75% probability that Clarity fails to become law this fall.”

TD Cowen said one likely outcome was for cloture to pass initially in September but then for Republicans to block Democratic amendments on the ethics and AML sections, leading Democrats to sink the second cloture vote.

It added that it was also likely no cloture vote ever happens. Cloture is the Senate’s procedural tool for ending debate on a bill so it can move to a final vote.

News dropped last week a vote on the bill would have to wait until lawmakers return from August recess. Bipartisan work has gone into the Clarity Act, which was passed by the House of Representatives last year, but some Republicans have accused Democrats of stalling the bill.

The bill, if passed, would be a federal rulebook for U.S. cryptocurrency markets. The latest draft of the Clarity Act contains language — drafted by Democrats and Republicans — banning government officials from promoting or making money from crypto. It started circulating in July.

Still, Democrats like Senator Elizabeth Warren, who has from the beginning criticized the Clarity Act, have claimed that new legislation will benefit the president and his family.

Major financial institutions — not just crypto companies — have backed the bill, including Goldman Sachs and Fidelity, as well as law enforcement groups.

This post TD Cowen Gives Crypto Clarity Act a 25% Chance of Passing This Fall first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

Bitcoin Magazine

Strategy Sells Bitcoin Again For Cash Buffer, STRC Buyback

Bitcoin treasury company Strategy on Monday announced that it again sold Bitcoin last week, and used the cash to buy back its preferred stock.

In a filing with the Securities and Exchange Commission, the Nasdaq-listed company said it sold 1,690 coins for $108.6 million, bringing its holdings to 840,447 coins, down from 842,138 it had the week before.

The cash, Strategy said, went to buying 1,152,020 STRC shares worth $109 million as part of a buyback program. STRC in June fell far below the $100 stated amount.

Strategy, which went from being an enterprise software company to buying Bitcoin in 2020, hasn’t bought any Bitcoin since June.

The company has reassured investors that selling Bitcoin is just part of its plan to grow its cash buffer. Strategy said Monday that it now holds $4.65 billion in cash.

Strategy’s stock (Nasdaq: MSTR) was trading nearly 3% lower on Monday. The stock has taken a hit since the price of Bitcoin nosedived last year. Investors buy MSTR to get amplified exposure to the biggest digital asset.

But now, as Bitcoin is nearly 50% below its October record, MSTR is down nearly 80% from the all-time high it notched last year.

Despite the sale, Strategy has maintained that its long-term posture toward Bitcoin hasn’t changed.

Strategy — formerly MicroStrategy — began buying Bitcoin in August 2020 as a treasury strategy to boost shareholder returns during the pandemic.

It has since spent more than $63.5 billion buying Bitcoin and remains by far the largest corporate holder of Bitcoin in the world.

Strategy’s approach spawned a wave of copycat companies that have since adopted similar crypto-treasury strategies of their own.

The company maintains that its long-term posture toward Bitcoin is still the same. CEO Phong Le he isn’t worried about the current bear market, and that the company plans to remain a long-term buyer of Bitcoin despite its recent sales.

This post Strategy Sells Bitcoin Again For Cash Buffer, STRC Buyback first appeared on Bitcoin Magazine and is written by Mathew Di Salvo.

CryptoSlate

Bitcoin trades near $64,000 heading into the most consequential US macro week of August, sitting almost on top of the market's largest nearby demand concentration.

The Aug. 12 inflation report, due less than 48 hours out, will help decide whether that floor holds or gets tested.

Glassnode's latest on-chain map puts that demand shelf at roughly $63,000, an area holding close to a tenth of Bitcoin's circulating supply. The market's repair test sits near $69,000, where recent buyers reach breakeven on their positions.

Why Wednesday matters

July's jobs report showed that payrolls fell by 23,000 against expectations for an 80,000 gain, and May and June were revised down by a combined 103,000. Traders repriced September hike odds down into the mid-to-high 40% range.

For the Aug. 12 CPI results, economists polled by Reuters expect headline inflation at 3.4% year-over-year and core inflation at 2.5%, both down from June's 3.5% and 2.6%, respectively.

A cooler print validates the case for a Fed pause, and a hotter one reopens the argument that inflation remains sticky even as hiring slows, the combination that keeps a central bank from stepping back.

Glassnode's July report identified the $63,000 shelf as the level at which roughly a tenth of the supply last changed hands, the heaviest concentration of buyers anywhere near the current price. The short-term holder cost basis, the average price recent buyers paid, is near $69,000.

Buyers who bought near the top of a prior rally and are still underwater tend to sell as soon as price lets them exit at cost, turning their own breakeven point into resistance. Glassnode says clearing it would thin Bitcoin's supply profile into what it calls an air pocket, with the next structural reference near $84,000.

| BTC level | Market meaning | Why it matters this week |

|---|---|---|

| $58K–$60K | Late-June recovery zone | Downside risk if the $63K shelf fails |

| $63K | Largest nearby demand shelf | Roughly one-tenth of supply last moved here; main support zone |

| $66K | Immediate range ceiling | First upside test if CPI comes in soft |

| $69K | Short-term-holder cost basis | Breakeven wall where recent buyers may sell |

| $84K | Next structural reference | Supply profile thins above $69K, creating upside “air pocket” risk |

Bitcoin's recovery is narrow

Glassnode's Aug. 10 update says Bitcoin has stabilized near $65,000, recovering from late-June lows around $58,000, with taker buying accelerating and perpetual taker activity running above its usual statistical range.

Institutional net flows are unusually strong, and the options skew has compressed, meaning traders are paying less for downside protection than before.

Centralized exchange turnover stays subdued, active addresses, transfer volume, and fees all sit near the lower end of their statistical range, and realized losses across the network still outweigh realized profits.

Treasury sells $58 billion of 3-year notes on Aug. 11, and Aug. 12 brings both the inflation print and a $42 billion 10-year note auction at 1 p.m. EDT, just hours apart.

Aug. 13 pairs the producer price index with a $25 billion 30-year auction, bringing the week's total Treasury supply to $125 billion.

Weak demand at either long-duration auction can keep yields elevated even if CPI itself comes in close to consensus. A soft inflation print paired with a poorly received 10-year auction would partly offset each other, while a hot print paired with weak demand would push both in the same direction.

| Date | Event | Market sensitivity | BTC relevance |

|---|---|---|---|

| Aug. 11 | $58B 3-year Treasury auction | Short/intermediate-rate demand | Sets early tone for Treasury supply |

| Aug. 12, 8:30 a.m. ET | July CPI | Inflation and Fed-hike pricing | Main directional catalyst |

| Aug. 12, 1 p.m. ET | $42B 10-year Treasury auction | Long-duration demand | Can amplify or offset CPI-driven yield move |

| Aug. 13, 8:30 a.m. ET | July PPI | Pipeline inflation | Confirms or challenges CPI signal |

| Aug. 13, 1 p.m. ET | $25B 30-year Treasury auction | Long-end yield pressure | Tests duration appetite after inflation data |

| Aug. 14 | July retail sales | Consumer strength | Confirms whether Fed can pause or must stay hawkish |

Why this reads as a liquidity story

Glassnode's mid-July macro read tied Bitcoin's recent weakness specifically to real yields, with the 10-year real yield near a 2026 high of 2.4%. Bitcoin's inverse relationship with the dollar has deepened over the same stretch, while its correlation with equities has eased.

The dollar index climbed to 99.76 ahead of the Aug. 12 print, and the 10-year Treasury yield is in the 4.66%-4.70% range. Both numbers move directly into Bitcoin's setup this week.

Aug. 14 brings July retail sales, and by the time it lands, CPI and Thursday's producer price index will have already set the market's read on inflation and the Fed's path.

Strong retail sales alongside a hot CPI would reinforce concern about a resilient consumer keeping prices elevated. Weak retail sales alongside a soft CPI would strengthen the case for a Fed pause.

How the week could resolve for Bitcoin

The bull case has CPI landing near or below consensus while the 10-year and 30-year auctions clear without a tail. Yields ease, the dollar softens, and Bitcoin uses the room to test $66,000 first.

A decisive move through the $69,000 cost basis, backed by real spot buying alongside the derivatives strength already in place, would open the thinner supply profile above it toward $84,000.

| Scenario | CPI / auction setup | Rates and dollar reaction | BTC level to watch | Article takeaway |

|---|---|---|---|---|

| Bull case | CPI at or below consensus; 10Y and 30Y auctions clear cleanly | Yields ease, dollar softens | $66K → $69K | BTC gets room to test the short-term-holder breakeven wall |

| Neutral case | CPI near consensus; auctions mixed but not disorderly | Rates stay range-bound | $63K–$66K | Stabilization continues, but breakout demand remains unproven |

| Bear case | Hot CPI or weak long-duration auctions | Yields rise, dollar strengthens | $63K | Demand shelf gets tested as macro support fades |

| Stress case | Hot CPI plus poor 10Y/30Y demand | Sharp long-yield repricing | $58K–$60K | Failure of $63K would turn the recovery into a failed repair attempt |

The bear case has CPI running hot, or the auctions landing poorly enough to keep long yields firm regardless of the inflation print. September hike odds climb back up, the dollar strengthens, and Bitcoin's tentative recovery loses the macro room it has been trading on.

A retest of the $63,000 shelf follows, and a clean break below it risks a slide back toward the $58,000 to $60,000 zone Bitcoin left behind in late June.

Bitcoin has spent weeks finding a floor near its biggest demand shelf. Aug. 12 decides whether that floor holds, or whether the shelf underneath it gets tested for real.

The post Bitcoin enters CPI week caught between a $63,000 on-chain demand zone and $69,000 holder resistance appeared first on CryptoSlate.

Grayscale withdrew its registration for the Cardano Trust ETF on Aug. 7, telling the SEC only that it “does not intend to proceed with the planned distribution.”

The move was voluntary and came along with parallel registrations for Hedera and Polkadot, within about three minutes of each other that same afternoon.

Two days later, ADA crossed a regulatory threshold that could have made its case for a spot ETF considerably easier. CME's regulated ADA futures had traded for six months as of Aug. 9, the track record the SEC's generic listing framework accepts as one path to spot-commodity ETP eligibility.

Cardano's only dedicated spot applicant walked away right before the rule that could have helped it took effect.

| Date | Event | Why it matters for ADA |

|---|---|---|

| Feb. 9, 2026 | CME ADA futures begin trading | Starts the six-month regulated futures clock |

| Aug. 7, 2026 | Grayscale withdraws Cardano Trust ETF registration | Removes the only dedicated U.S. spot ADA ETF filing |

| Aug. 7, 2026 | Grayscale also withdraws HBAR and DOT filings | Suggests broader product-priority decision, not necessarily an ADA-specific issue |

| Aug. 9, 2026 | ADA reaches six months of CME futures history | ADA crosses a key eligibility route under generic listing standards |

| After Aug. 9 | No other dedicated U.S. spot ADA filing appears active | ADA becomes eligible-looking but sponsorless |

What is fact and what is inference

Other Grayscale altcoin registrations, including Bittensor, Aave, BNB, NEAR, and Zcash, remained active and preliminary the next day. That pattern points to a portfolio-level product decision, though Grayscale has not confirmed why it walked away.

ADA has also fallen more than 41% year-to-date and roughly 70% since Grayscale's original ETF filing. That decline fits a broader story about shrinking appetite for altcoin products, but it does not confirm what Grayscale was weighing when it pulled the filing.

The registration of the Grayscale Cardano Trust ETF never became effective, and the filing states plainly that no securities were issued or sold under it. There was no operating fund holding ADA, so there was nothing to unwind.

The only dedicated US spot ETF application built to hold ADA itself is gone. A vehicle like that would have allowed brokerage and institutional demand to convert directly into ADA purchases every time new shares were created.

With Grayscale gone and no other single-asset spot filing currently on record, ADA is missing that specific demand channel until a new sponsor steps in.

Why futures funds and baskets fall short

Volatility Shares runs a Cardano ETF built primarily on CME ADA futures, and its prospectus states that the fund does not invest directly in ADA.

Its combined net assets across both the standard and leveraged versions totaled roughly $1.26 million as of July, a small amount relative to ADA's roughly $7.1 billion market cap.

Grayscale's CoinDesk Crypto 5 ETF dropped ADA in its January rebalance, replacing it with BNB once the underlying index reselected its five components. Franklin Templeton's Crypto Index ETF still holds ADA, but at just 0.69% of net assets, about $70,709 worth as of the end of last year. Neither structure lets ADA demand flow in on its own terms.

| Investment wrapper | Holds ADA directly? | Let's ADA demand stand alone? | Investment-instrument takeaway |

|---|---|---|---|

| Dedicated spot ADA ETF | Yes | Yes | Would convert fund demand into direct ADA exposure |

| ADA futures ETF | No | Partly | Brokerable exposure, but demand flows through futures, not spot ADA |

| Leveraged ADA futures ETF | No | Partly | Trading product, not a long-term spot allocation wrapper |

| Multi-crypto index ETF | Sometimes | No | ADA can be included, reduced, or removed by index rules |

| Direct ADA ownership | Yes | Yes | Pure exposure, but outside the ETF/brokerage wrapper thesis |

A $25 million ADA ETF would represent about 0.35% of ADA's current market cap; a $100 million fund would reach roughly 1.4%; a $250 million fund would approach 3.5%, and a $500 million fund would cross 7%, enough to make ADA a visible allocation product on its own.

Creations, hedging, and secondary trading all complicate the relationship, but they show the size of the demand channel that just went quiet.

Under the SEC's generic listing standards, qualifying commodity-based trust shares can list without the exchange first filing a separate Section 19(b) proposed rule change for that individual product.

That removes the bespoke 19b-4 review track, which under Exchange Act Section 19(b)(2) can run from an initial 45-day review period to as long as 240 days if proceedings are instituted and extended.

Cardano's six-month futures history put ADA in a position to use that faster path.

Which way Cardano's investability goes

The bull case has another issuer filing on the strength of ADA's now-qualifying futures history, using the same six-month CME track record Grayscale had access to.

A new spot application inherits a faster review window and does not have to rebuild the regulatory case from zero. Grayscale's exit becomes a handoff between sponsors, and ADA regains a path toward the demand channel a dedicated ETF represents.

The bear case has issuers directing their attention toward tokens with clearer demand, Solana, XRP, Dogecoin, and BNB among them, leaving Cardano without a sponsor willing to file.

| Hypothetical spot ADA ETF size | Share of ADA’s ~$7.1B market cap | What it would signal |

|---|---|---|

| $25M | ~0.35% | Small but visible institutional wrapper |

| $100M | ~1.4% | Meaningful standalone ADA allocation product |

| $250M | ~3.5% | Clear evidence of institutional/brokerage appetite |

| $500M | ~7.0% | ADA becomes a visible ETF allocation category |

Futures wrappers stay near their current size, multi-asset baskets keep ADA at a small weight or drop it entirely, and the market starts reading the missing spot filing as a signal about ADA's institutional standing.

Cardano cleared the regulatory bar built to make a spot ETF possible. Whether ADA becomes an easier asset to invest in now depends on whether anyone else decides that bar is worth clearing.

The post Cardano finally cleared the SEC shortcut for a spot ETF, but its last remaining sponsor quit two days too early appeared first on CryptoSlate.

Standard Chartered initiated coverage of Chainlink (LINK) with a $200 price target for 2030, laying out a staged path to get there: $13 by the end of this year, $41 in 2027, $82 in 2028, $133 in 2029, and $200 in 2030.

LINK trades near $7.47 today, meaning the 2030 target implies roughly 27 times the current price. Even the bank's nearest milestone, the $13 call for the end of 2026, sits about 74% above LINK's current price.

The firm previously shared a $3,500 target for AAVE, which is close to 50 times the $70 initiation price. UNI carries a $100 target against an initiation price near $2.50 to $2.70, and MORPHO carries a $60 target against a coverage price near $2.13.

Every one of the four implies returns in the 25 to 50 times range.

| Token | Standard Chartered target | Reference price | Implied upside | Core infrastructure role |

|---|---|---|---|---|

| LINK | $200 by 2030 | ~$7.47 today | ~27x | Oracles, data feeds, CCIP, tokenization connectivity |

| AAVE | $3,500 by 2030 | ~$70 at initiation | ~50x | DeFi lending and collateral markets |

| UNI | $100 by 2030 | ~$2.50–$2.70 at initiation | ~37x–40x | Decentralized liquidity |

| MORPHO | $60 by 2030 | ~$2.13 at coverage | ~28x | Lending vaults and on-chain credit infrastructure |

The $4 trillion assumption behind the LINK prediction

The bank expects tokenized assets to grow from about $340 billion today to $4 trillion by the end of 2028, with assets deployed in decentralized finance expanding 37 times to $2.7 trillion by 2030.

For Chainlink specifically, the bank expects fees to rise roughly 25 times as that tokenized activity grows.

Chainlink already secures more value than any other oracle network, with Standard Chartered's note putting total value secured above $110 billion, roughly 70% of oracle-dependent DeFi value globally and more than 80% on Ethereum. Aave V3 alone accounts for 44% of that secured value.

The bank's analyst Geoff Kendrick named Swift, DTCC, Euroclear, JPMorgan, Mastercard, UBS, Fidelity, and S&P Global among the institutions already using Chainlink's services.

He argues that tokenized funds and bonds need net asset values, interest rate data, and reserve attestations. Off-chain customers paying for that data should become a larger share of Chainlink's fees over time.

More than $7 billion in token value has moved from legacy bridges to Chainlink's CCIP since the April exploit on KelpDAO's multichain infrastructure. CCIP volume reached $4.9 billion in the second quarter, up 353% year over year.

| Assumption | Standard Chartered / Chainlink data point | Why it matters for LINK |

|---|---|---|

| Tokenized assets expand | ~$340B today to $4T by end-2028 | More assets need pricing, data, NAVs, and attestations |

| DeFi assets grow | 37x to $2.7T by 2030 | More collateral and lending activity depend on oracle data |

| Chainlink fees rise | Roughly 25x expected increase | Fee growth is the bridge from usage to LINK value |

| Oracle dominance holds | More than $110B total value secured | Gives Chainlink leverage to tokenization growth |

| CCIP adoption expands | $4.9B Q2 volume, up 353% YoY | Positions Chainlink as cross-chain infrastructure, not just an oracle |

The last three times Standard Chartered did this

Following Standard Chartered predictions, UNI rose 22.5% around the bank's $100 call, MORPHO traded more than 13% higher over 24 hours around its $60 target, and AAVE gained 5.6% around the $3,500 initiation.

Broader crypto conditions moved alongside each report too, so the moves coincided with the calls without proof that the calls caused them.

LINK traded at $8.27, down 0.8% on the day, right around the time Standard Chartered published its note. Traders may be skeptical of Chainlink's path from usage to token value, or the $200 call may have already been partly priced in.

LINK may react on a longer delay than UNI or MORPHO did.

Standard Chartered's math assumes that tokenization growth directly translates into higher LINK value. Chainlink's own economics documentation states that its Reserve accumulates LINK through both off-chain enterprise revenue and on-chain service usage, a mechanism intended to bridge institutional adoption and token demand.

Whether that bridge actually holds is the entire bet Standard Chartered is making, since Chainlink could become widely used infrastructure without much of that value ever reaching LINK holders.

What decides whether the pattern repeats

The bull case has traders eventually doing with LINK what they did with UNI and MORPHO, rotating in as CCIP volume keeps climbing and more tokenization headlines reinforce the thesis.

LINK moves toward the $13 to $25 range over the next six to twelve months and starts trading as a tokenization-beta asset. The delayed initial reaction sets up a later move.

The bear case has Chainlink's institutional usage staying exactly that, usage, without turning into fees and reserve accumulation large enough to move the token.

| Scenario | What has to happen | LINK price path | What it would prove |

|---|---|---|---|

| Bull case | Traders rotate into LINK as CCIP volume and tokenization headlines keep building | $13–$25 over 6–12 months | LINK starts trading as a tokenization-beta asset |

| Delayed reaction case | Market waits for evidence that institutional usage drives fees and reserve accumulation | Gradual move toward $13 | The Standard Chartered effect works slower for LINK than for UNI or MORPHO |

| Bear case | Chainlink usage grows, but token value capture remains unclear | $5–$8 range | Chainlink can succeed as infrastructure without LINK rerating |

| 2030 thesis case | Tokenized assets approach $4T and Chainlink captures meaningful fee growth | $82–$200 by 2028–2030 | The market accepts Standard Chartered’s value-accrual model |

Competitors take share of the oracle and data market, and enterprise clients keep paying without that value reaching LINK holders in a meaningful way. The token remains range-bound between $5 and $8, while the underlying network continues to expand regardless.

Chainlink already sits underneath more tokenized value than any other oracle network. Whether that translates into a $200 token depends on whether the market ever agrees to price in the value-accrual story Standard Chartered just told.

The post LINK could be next in line after Standard Chartered’s UNI and AAVE targets sparked sharp repricings appeared first on CryptoSlate.

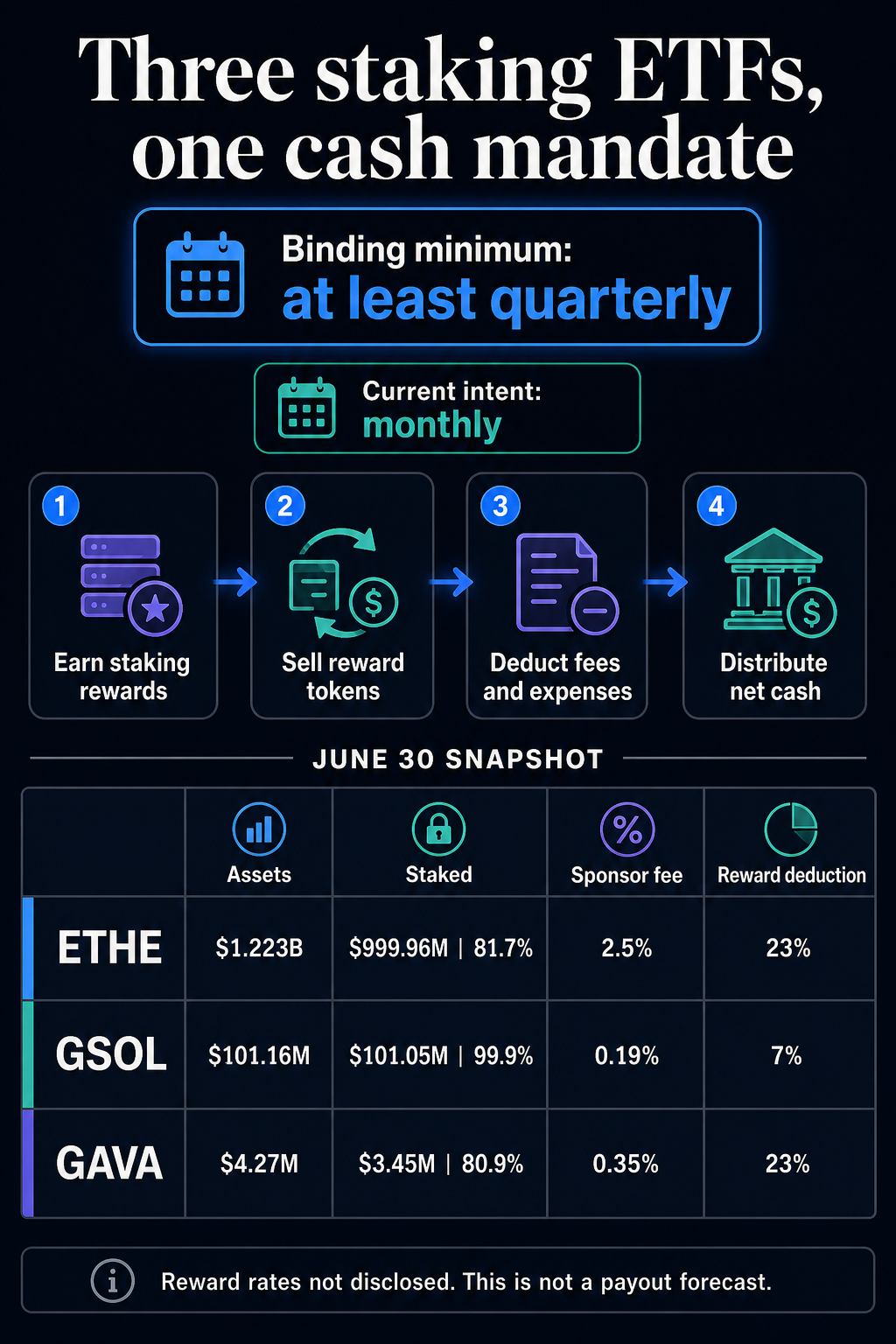

Grayscale has formalized a mandatory minimum cadence for converting staking rewards from three crypto exchange-traded products into cash and paying the net proceeds to shareholders.

Trust amendments executed Aug. 6 for the Grayscale Ethereum Staking ETF (ETHE), Grayscale Solana Staking ETF (GSOL) and Grayscale Avalanche Staking ETF (GAVA) require each product to reduce “Staking Consideration” to cash no less often than quarterly. Net proceeds must then be distributed promptly after applicable fees and trust expenses.

The three trusts currently intend to make distributions monthly, according to Form 8-K filings submitted Aug. 7, but the binding floor is quarterly.

As the trusts receive staking rewards, they must periodically sell that earned consideration and pass the resulting cash to investors. The rule therefore creates a recurring market sell flow for reward tokens.

It does not create scheduled liquidation of the trusts’ principal ETH, SOL or AVAX holdings. The distribution clauses apply to staking consideration earned by the products. Other disclosures still permit token sales for separate purposes, including redemptions, fees and expenses.

The amendments establish that reward tokens will be converted, but not how much will be sold in any future period.

As of June 30, ETHE reported $1.22 billion in total assets and $999.96 million in staked ETH, equivalent to roughly 81.7% of its assets. GSOL reported $101.16 million in assets and $101.05 million of staked SOL, or about 99.9%. GAVA reported $4.27 million in assets and $3.45 million of staked AVAX, or about 80.9%.

The reports do not provide current annualized reward rates. Future sales and payouts will depend on rewards actually received, the amount staked, protocol-level reward rates, token prices, and deductions.

ETHE charged a 2.5% annual Sponsor fee, while its Sponsor staking fee and validator fees together accounted for 23% of gross rewards as of June 30. GAVA disclosed a 0.35% annual Sponsor fee and the same 23% aggregate reward deduction. GSOL disclosed a 0.19% annual Sponsor fee and a 7% aggregate staking-related deduction covering Sponsor and validator fees.

The annual Sponsor fees and the reward deductions use different bases and should not be treated as additive percentages.

ETHE offers an operating precedent without a forecast. The fund paid approximately $9.4 million, or $0.083178 per share, on Jan. 6 after selling staking rewards earned from Oct. 6 through Dec. 31, 2025. Different asset levels, staking participation, fees, reward rates, and token prices make it unsafe to extrapolate that payment across the three products.

Grayscale move creates a tax complexity

The conversion to cash planned by Grayscale may simplify what shareholders receive, but ETHE and GSOL tax disclosures indicate that the underlying activity can create multiple potential tax consequences.

Assuming grantor-trust treatment applies, a US holder is generally treated as receiving a pro rata share of staking income when the trust earns it.

A subsequent trust sale of reward tokens to fund a cash distribution can also allocate a pro rata capital gain or loss to the holder. Under the treatment described in the filings, receiving the cash itself should not be an additional taxable event.

The disclosures caution that the grantor-trust position is not guaranteed. They also flag potential unrelated business taxable income for some tax-exempt holders and unresolved sourcing or withholding questions for non-US investors.

The amendments therefore create a recurring operational loop: earn reward tokens, sell them, and distribute net cash. Its market sell flow will depend on realized rewards and deductions, not headline asset totals alone.

The post Grayscale turned more than $1.1 billion of staked crypto into a recurring reward-sale machine for ETF holders appeared first on CryptoSlate.

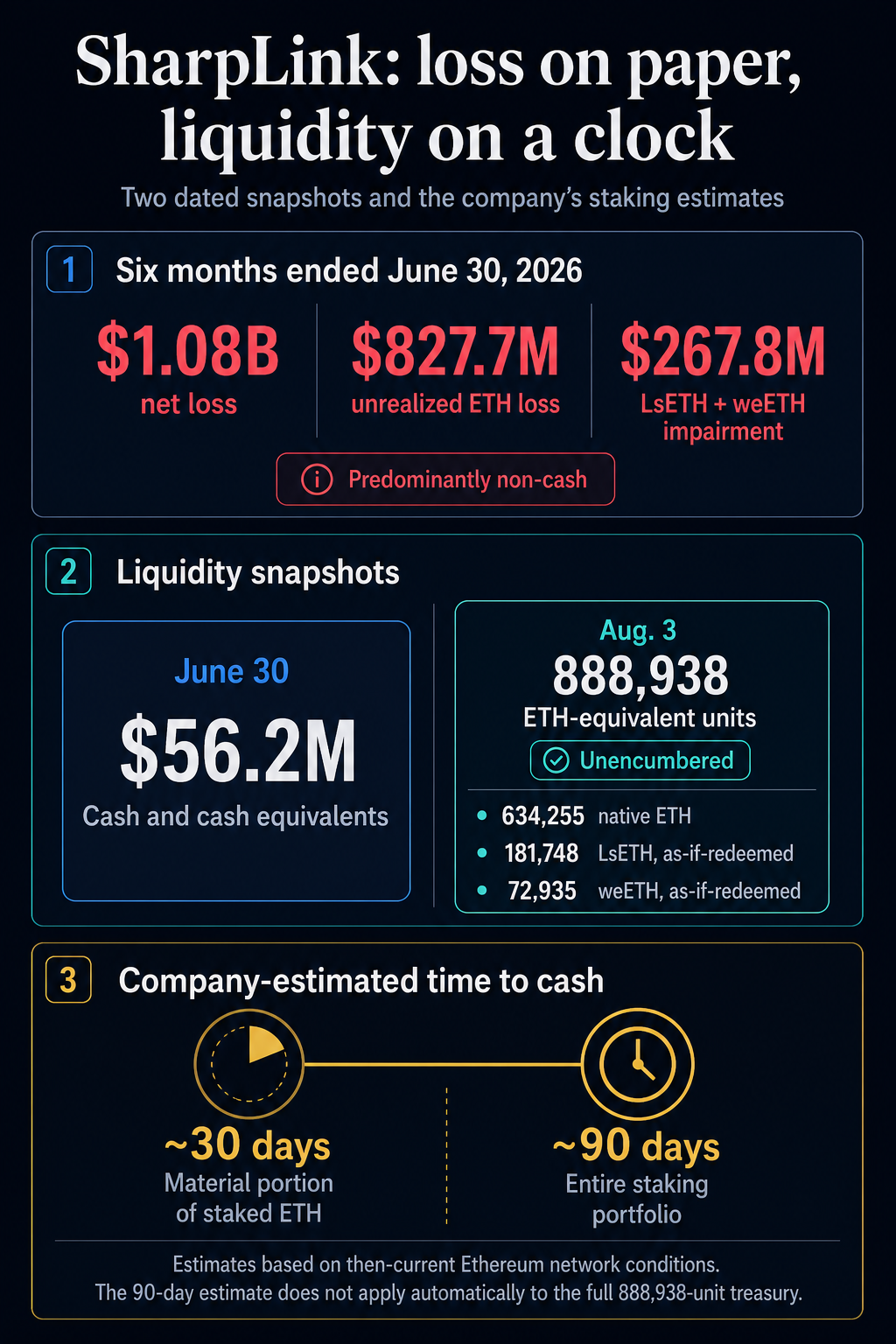

Ethereum treasury company SharpLink reported a $1.08 billion net loss for the six months ended June 30. Its Aug. 7 quarterly filing attributes most of that result to price-related accounting charges. Much of the company’s treasury is staked, making conversion time a material part of its liquidity profile.

The filing attributes $827.7 million of the loss to an unrealized decline in the value of ETH and another $267.8 million to impairments of LsETH and weETH, tokens representing liquid staking and restaking positions. Those predominantly non-cash charges exceeded the net loss because other results partly offset them.

The six-month loss was 934.3% above the roughly $104.4 million recorded a year earlier. The comparison spans different operating profiles because SharpLink launched its ETH treasury strategy on June 2, 2025, near the end of the earlier period.

What Ethereum can become cash, and when

SharpLink held $56.2 million in cash and cash equivalents at June 30. In a separately dated snapshot, it reported 888,938 unencumbered ETH-equivalent units as of Aug. 3: 634,255 native ETH, 181,748 ETH on an as-if-redeemed basis from LsETH and 72,935 ETH on the same basis from weETH.

ETH traded at $1,916.57 as of Aug. 10, giving the Aug. 3 count an illustrative gross mark of roughly $1.7 billion. That mark mixes dates and includes as-if-redeemed staking positions, so cash proceeds would depend on redemption timing and sale prices.

SharpLink estimates that, under Ethereum network conditions at the time of the filing, a material portion of its staked ETH could be withdrawn and converted to cash in about 30 days.

The company puts the entire staking portfolio at about 90 days, and the filing states the 90-day timing for the staking portfolio and separately reports 888,938 ETH-equivalent units in the total treasury.

Ethereum validator exits vary with network demand and require sweep processing after exit. LsETH redemptions can require validator exits when protocol liquidity is insufficient, while weETH withdrawals can face network-dependent delays despite having no fixed lock period.

SharpLink’s common shares issued and outstanding increased 10.3% to 216.98 million at June 30 from 196.71 million at the end of 2025. In June, the company raised about $75 million gross by selling 10,013,351 shares with accompanying warrants at a combined purchase price of $7.49 per package.

It used part of the proceeds to buy 10,000 ETH for about $16.1 million and repurchased 2.13 million shares.

SharpLink describes its unencumbered crypto assets as additional liquidity support beyond cash. The filing also warns that stressed markets could impede sales or force unfavorable pricing, and its liquidity depends on both conversion time and the price available when cash is needed.

The post SharpLink posts $1B loss as its $1.7B Ethereum treasury could take 90 days to fully convert to cash appeared first on CryptoSlate.

CryptoTicker.io

Since 1 July 2026, crypto service providers in the European Union may only operate if they hold an authorisation under the MiCA regulation. Anyone who failed to obtain one by that date has to wind down their EU business and ask customers to withdraw their balances. A wave of fraud has grown out of exactly that: tens of thousands of investors across Europe are right now receiving a perfectly legitimate message telling them to move their money elsewhere. For criminals this is the most convenient starting position in years, because their own demand no longer has to sound plausible. It only has to look genuine.

Supervisors in several EU member states have issued warnings over the past few days. According to the French markets regulator AMF, quoted in international reporting on 5 and 6 August, perpetrators pose as staff of supervisory authorities or licensed trading venues and instruct customers of unauthorised providers to move their holdings urgently. Stéphane Pontoizeau, who covers this area at the AMF, is quoted as saying that the current moment offers fraudsters a better opportunity than usual. The same reports note that ESMA has found its own name and logo being misused in letters of this kind.

This article is written as a checklist: how to recognise a genuine withdrawal request, which two registers you need for that, and what to do if your provider really is winding down.

Why crypto phishing works so well after the MiCA deadline

Fraud in the crypto market normally depends on talking a victim into an action they would never take on their own. A stranger writes that there is a security problem and that the balance has to move to a safe wallet immediately. Anyone who has read about this before grows suspicious, because the request comes out of nowhere.

In the summer of 2026 that layer of protection is missing. The request does not come out of nowhere. It is the routine process that the supervisors themselves ordered. According to reporting on the state of the register, around 323 companies have received a MiCA authorisation, while more than 1,700 others have to stop doing business in the EU. Those figures come from analyses at the end of July and keep shifting, because further authorisations are still coming through. In our own review of the register, only 21 of those entries were trading platforms in the narrower sense, meaning providers where retail investors actually buy and sell. How it came to that is set out in our analysis of the MiCA register.

The result is a window in which a great many people are all expecting a legitimate message that tells them to move their money. The AMF says it deliberately avoided short wind-down deadlines, because time pressure drives those affected straight into the hands of the perpetrators. After this week, that is the most important point for you: a genuine wind-down gives you time. If something is rushing you, that alone is the warning signal.

What a fake withdrawal request looks like

The letters that have reached the authorities are well made. What has been described includes rebuilt websites that follow a genuine provider or authority down to the layout, documents carrying copied letterheads and file references, messages from supposed officials, and transfer instructions pointing to wallets that belong to the perpetrators. Phone calls come on top of that.

What is striking is what these letters regularly leave out. They rarely give the file reference of a wind-down, they do not point to a register entry you could look up yourself, and they give you no route by which to reach the sender independently. What they do supply is a destination address and a reason to hurry.

A second variant is more subtle. Instead of a wallet address you receive a link to a platform that is supposedly MiCA-licensed. You open an account there, you even verify yourself with an ID document, and you then see your balance as a number on an interface that belongs to the operators. Withdrawals subsequently fail because of alleged taxes. This version is the more dangerous one, because it copies the familiar process of opening an account.

The register test: is the crypto exchange MiCA-licensed at all?

There is one check that settles the great majority of these cases, and it costs you two minutes: look the provider up in an official register, using an address you type in yourself rather than a link from the message.

The reason is straightforward. Fraudsters can send any claim, rebuild any logo and fake any confirmation page. What they cannot do is create an entry in a supervisory authority's database. If a supposedly licensed provider is not in there, the matter is settled, however convincing the letter looks.

The ESMA register: every MiCA authorisation in the EU

The European securities regulator maintains the central directory of all service providers authorised under MiCA. It shows you whether a company holds an authorisation, which member state granted it and which services it covers. A provider may well be authorised without that authorisation covering every activity. Open the ESMA MiCA register and search for the legal entity name, not the brand. Many trading venues operate under a brand name but are registered under a different company. If the message gives no company name at all, that too is a finding.

The BaFin database: crypto custody and trading in Germany

For providers holding a German authorisation, the Federal Financial Supervisory Authority maintains its own company database. It is the faster route if your provider is based in Germany, and it additionally shows which permission was granted. The BaFin company database can be used without registering.

Both registers, however, only answer the question of whether a company is authorised, not the question of whether your email really came from that company. Hence the second step.

Second step: reach the provider through the official channel

Once you know the provider exists, you check whether the message came from it. A single rule applies here, and it is less comfortable than it sounds: you use no contact route whatsoever taken from the message. No telephone number from the email, no link, no attached PDF, no QR code.

Instead you open the app you already have on your phone, or you type in the provider's domain yourself. If there is no notice about a wind-down inside the logged-in area, then as far as you are concerned that wind-down does not exist. A company telling its EU customers to withdraw does so in the account itself, precisely because it fears this kind of confusion.

Authorities, incidentally, virtually never write to retail investors directly in such cases. Neither BaFin nor ESMA will email you asking you to move balances to a particular address. A message that does exactly that while looking official can be treated as a forgery without any further checking.

Language markers: how to spot a phishing email in the text

If you have a message in front of you and cannot reach the registers at that moment, a handful of markers will help. None of them is proof on its own, but together they paint a clear picture.

- A specific destination address in the text. Genuine wind-down notices describe routes, not wallets. If a recipient address appears in the message, that is the clearest indication there is.

- A deadline of a few days or hours. Wind-downs under MiCA run over weeks and months.

- A new contact channel. If the conversation moves to a messenger when everything so far arrived by email, something is wrong.

- A request for login credentials or the recovery phrase. There is no legitimate process in which anybody needs your twelve or twenty-four words.

- A domain that is almost right. An extra hyphen, a different ending, one letter swapped. Compare it character by character against your password manager.

- Fees payable before the withdrawal. If you are asked to pay in order to reach your own balance, the case is clear.

Conversely, a professional appearance is not a mark of authenticity. The forgeries the supervisors are warning about are a problem precisely because they are well made. Spelling mistakes as a giveaway are advice from an earlier era.

When your crypto exchange really does close its EU business

Suppose the check comes out like this: the message is genuine, your provider did not receive a MiCA authorisation and is closing its EU business. You then have a real but solvable problem. The order matters, because a wrong first step gets expensive.

Secure your paperwork first. Download transaction histories, account statements and tax reports while you still have access. Once the service is switched off you often only reach that data through written requests, and you need it for your German tax return: the acquisition date and acquisition cost of every position decide whether a later sale falls under the one-year holding period.

Only then do you look for a destination. An authorised trading venue is the obvious choice if you want to carry on trading; which providers cleared the MiCA hurdle and how they differ on fees and custody is set out in our comparison of regulated crypto exchanges. If you intend to hold for the long run anyway, self-custody is the alternative that makes you independent of the authorisation question.

Only after that do you move any balance, and you do it with a test amount. Send a small sum, wait for it to arrive and transfer the rest afterwards. That costs one extra network fee and protects you from the most expensive mistake of all, the wrongly copied address.

One note on tax: a pure transfer between two accounts that both belong to you is not a disposal and triggers no tax in Germany. Selling because the provider only pays out in euro, by contrast, is a taxable event. So check beforehand whether it hands over the coins themselves.

Crypto sent and fraud noticed: what still helps

A crypto transfer cannot be reversed. Anyone promising you otherwise on the telephone belongs to the second wave: so-called recovery services, which get in touch after a loss and offer to retrieve the funds against an advance payment, are a well-documented fraud pattern in their own right.

Plenty is still worth doing. File a report with the police, because investigators piece addresses together and exchanges can freeze blocked funds when a withdrawal is attempted. Report the incident to BaFin. Preserve messages, domains and transaction hashes before the other side shuts its infrastructure down. And change the passwords and two-factor methods of every account you logged into on the fake site.

What changes permanently for crypto investors in the EU

For you, the licensing requirement leaves behind a habit that outlasts this summer: before you deposit money with a provider, you look it up in the register. That was hard before MiCA, because there was no single directory. Since this year it is one search query. Anyone wanting to follow the market clear-out in context will find the wider picture in our analysis of the winners and losers of the MiCA deadline.

Transparency note: in our comparisons we assess providers with some of whom partnerships exist. This has no bearing on the checks described here; the registers linked above are official directories.

What to take away

- Check the provider in the register before you move anything. Type the address of the ESMA register or the BaFin database in yourself and search for the legal entity name. If it is not there, the message is dealt with. Which authorised trading venues are open to you is shown in our comparison of regulated crypto exchanges.

- Confirm every withdrawal request inside your logged-in account. Open the app or the website by your own route, never through a link from the message. If no notice is waiting there, you do nothing. If you are switching anyway, our overview of crypto exchanges compared will help you choose.

- Move your holdings into self-custody if you intend to hold for the long run. That way you no longer depend on any service provider's authorisation. Which device is suitable and what matters for the backup is covered in our hardware wallet comparison. Here too, send a test amount first.

(As of August 7, 2026. This article is not investment advice. Prices and fee structures change; check the terms with the provider before you buy.)

Transparency note: This article was produced with the assistance of artificial intelligence and reviewed by our editorial team before publication. All figures and claims were checked against the primary sources linked in the text. The feature image was generated with AI.

The SEC has scheduled an open meeting for Friday, August 14, 2026 at 10:00 a.m. ET, and there is exactly one item on the agenda: whether to propose new rules creating a tailored offering regime for certain investment contracts involving crypto assets.

That is Regulation Crypto. It is the first formal SEC crypto rulemaking of Chairman Paul Atkins' tenure, and the notice landed Monday night with unusually short lead time.

What exactly is the SEC voting on?

Not a finished rule. Friday's vote decides whether to publish the proposal and open it for public comment. The three-member, all-Republican commission is expected to green-light that step.

The meeting runs from the Commission's Washington headquarters and will be webcast on sec.gov.

What would Regulation Crypto actually change?

Based on the framework Atkins laid out in March, the proposal is expected to give crypto projects a route to raise capital without triggering full securities registration, plus an exit path out of SEC jurisdiction once a team is no longer actively managing the network.

Earlier reporting on the draft pointed to capped raises for early-stage issuers and a multi-year exemption window. Those numbers are not confirmed until the text is public on Friday.

The bigger point is durability. Everything the agency has issued so far on crypto has been staff statements and policy guidance, which the next chairman can erase in an afternoon. A rule in the Federal Register cannot be undone without another full rulemaking cycle.

Does this mean the CLARITY Act is dead?

No, but it is late. The Senate left for August recess without a vote on the CLARITY Act. Majority Leader John Thune filed cloture on the motion to proceed on August 8, which sets the first procedural vote for 2:15 p.m. ET on Tuesday, September 15.

That vote needs 60 senators. If it fails, the bill loses its realistic path for 2026. Open fights remain over illicit-finance provisions, stablecoin yield and government ethics language.

Analysts read Friday's meeting as the SEC moving on without Congress. TD Cowen described it as the first of several rulemakings the agency will run to deliver certainty after the Senate stalled.

When do these rules actually bite?

Not soon. A proposal opens a comment period that typically runs two to three months, followed by a rewrite before any final adoption. Realistically this is a 2027 story for compliance teams.

For markets, the signal matters more than the timeline. Washington now has two tracks running in parallel, and only one of them needs 60 votes.

Bitcoin Bought Before March 2021: When a Sale in Austria Can Still Be Tax-Free

Anyone who bought Bitcoin before March 2021 may hold a considerable tax advantage in Austria. Gains on newer Bitcoin holdings are generally taxed at 27.5 percent, but older coins fall under transitional rules. The decisive date is February 28, 2021: cryptocurrencies acquired up to that day generally count as legacy holdings. The Austrian crypto tax regime in force since March 2022 does not automatically extend to those coins.

Why Old Bitcoin Can Be Sold Tax-Free in Austria

Before the crypto tax reform, privately held Bitcoin was generally treated under the rules for speculative transactions. A sale was taxable above all where no more than a year had passed between acquisition and disposal. Once that period had elapsed, the sale could generally take place tax-free.

Take an investor who bought Bitcoin in 2020 and has held it unchanged ever since. The one-year speculative period that applied at the time expired long ago. A sale in 2026 can therefore be tax-free in principle, even if the Bitcoin price has multiplied since the purchase.

Example:

Bitcoin purchase in 2020: 10,000 euros

Sale in 2026: 80,000 euros

Increase in value: 70,000 euros

If the coins genuinely still qualify as private legacy holdings and no special rules apply, that gain can remain tax-free in Austria in principle. Had the same Bitcoin been bought after February 28, 2021, the identical increase in value would generally fall under the new crypto tax regime and, as a rule, under the special tax rate of 27.5 percent.

An Intervening Swap Can End Legacy Status

The transaction history is what matters most here. The question is not whether the investor has been “invested in crypto” since 2020, but whether the precise coins being sold today still trace back to a purchase made before March 2021.

Under the old legal framework, swapping Bitcoin for another cryptocurrency also counts as a disposal. Say old Bitcoin was swapped for Ether in 2023. The disposal of the old Bitcoin can still be tax-free, because the speculative period had expired long before. The Ether acquired in that swap, however, dates from 2023 and therefore forms new holdings.

The Austrian finance ministry confirmed as much in 2025 for a comparable token swap: where the speculative period on the legacy holding has already expired, its hidden reserves are not taxed, and the cryptocurrencies received in exchange count as new holdings from that point on.

An old purchase receipt on its own is therefore not enough. Investors have to be able to trace the entire chain through to the coins they hold today.

Legacy and New Holdings in the Same Wallet

Things get complicated when a single wallet holds Bitcoin bought in 2020 alongside coins bought later. The Austrian cryptocurrency ordinance generally allows the holder to choose which units count as sold in a disposal. Where no choice is made, the unit acquired earlier is treated as sold first in case of doubt.

In practice that can make a substantial difference.

An investor holding 0.5 BTC from 2020 and a further 0.5 BTC from 2024 who then sells 0.5 BTC should document which holding is being disposed of. Otherwise the exchange and the investor may reach different conclusions on the tax treatment.

Take Care With Lending and Other Crypto Income

Legacy holdings also become more complicated where the Bitcoin has been used to generate ongoing crypto income.

An investor who used old Bitcoin for lending after February 2022 already falls under the new crypto tax regime as regards the ongoing income earned from it. The cryptocurrencies newly acquired in this way count as new holdings. The fact that the Bitcoin originally deployed is old does not automatically extend legacy status to the lending rewards.

On April 28, 2026 the Federal Finance Court also decided a relevant case on the interest-bearing investment of cryptocurrencies before the new crypto tax law took effect. The court concluded that lending at that time qualified as another service rather than as a classic transfer of capital under section 27(2) of the Austrian Income Tax Act. An official appeal has been lodged against the ruling, so the legal question is not yet finally settled.

For old Bitcoin with a lending history, a blanket claim that legacy holdings are tax-free is therefore inadvisable.

Documentation Becomes the Decisive Factor

Anyone planning to sell a larger legacy holding tax-free in 2026 should be able to show that the Bitcoin in question was acquired on February 28, 2021 at the latest and that no new acquisition has taken place for tax purposes since.

The following records matter in particular:

- purchase statements from the original exchange,

- bank transfers relating to the Bitcoin purchase at the time,

- wallet addresses and blockchain transactions,

- CSV exports from old exchange accounts,

- evidence of wallet-to-wallet transfers,

- earlier crypto-to-crypto swaps,

- documents on lending or other yield models.

Where legacy and new holdings are mixed, investors should also document which Bitcoin was allocated to the sale.

Conclusion

Anyone who bought Bitcoin on February 28, 2021 at the latest and has held it as a private legacy holding can in principle still sell those coins tax-free in Austria in 2026. The new flat-rate taxation of crypto gains at 27.5 percent does not apply automatically to such legacy holdings.

The history is what decides the matter. Swaps made in the meantime can produce newly acquired cryptocurrencies, lending rewards count as new holdings under certain conditions, and with mixed wallets it has to be established which units were actually sold.

Where values have risen sharply, the problem is therefore less today's Bitcoin price than the question of whether the legacy holding can still be documented without gaps after five years or more.

(As of August 11, 2026. This article is not investment advice. Prices and fee structures change; check the terms with the provider before you buy.)

Transparency note: This article was produced with the assistance of artificial intelligence and reviewed by our editorial team before publication. All figures and claims were checked against the primary sources linked in the text. The feature image was generated with AI.

Holding Bitcoin as a Business Owner: Private or Business Assets?

Business owners in Austria do not have to allocate Bitcoin to business assets automatically. What matters is the purpose the cryptocurrency actually serves. If it is held purely as a personal investment, it can generally remain private property. Where there is a clear link to the business activity, much points towards business assets. The classification has direct consequences for taxation, bookkeeping and the offsetting of losses.

When Do Bitcoin Count as Business Assets?

Bitcoin are likely to be business assets where a company:

- receives them as payment for goods or services,

- uses them regularly for business payments,

- holds them as part of a crypto, mining or trading operation,

- deliberately deploys them as part of a corporate treasury strategy.

If a self-employed consultant buys Bitcoin purely as a private investment, by contrast, the coins do not become business assets simply because the purchase went through the business account. The decisive factor is the actual business function. The source of the payment or the label on a wallet are only indications.

Sole Traders and Limited Companies Are Treated Differently

In a sole proprietorship the owner and the private individual are legally the same person. For tax purposes, private and business assets still have to be kept apart. The position differs for a limited company (GmbH): Bitcoin bought by the company or received as a customer payment belong to the company. The shareholder may not simply move them to a private wallet. Private use of company assets can be treated as a hidden distribution and trigger additional tax.

What Tax Applies When Business Bitcoin Are Sold?

For sole traders, gains on Bitcoin held as business assets can in principle also fall under the special tax rate of 27.5 percent. That does not apply without limits. Where crypto trading or mining forms the core of the business activity, the gains may be taxed at the ordinary progressive income tax rate. In a limited company, profits are first subject to corporation tax. If they are later distributed to the shareholder, capital gains tax can apply on top.

Moving Bitcoin to a Private Wallet Can Be Taxable

Anyone who permanently moves business Bitcoin into private assets makes a withdrawal for tax purposes. This is generally valued at the current market price.

Example:

- Business acquisition cost: 15,000 euros

- Market value at withdrawal: 40,000 euros

- Possible business gain: 25,000 euros

A pure transfer between two business wallets, on the other hand, is generally not a taxable sale. The business allocation does have to remain documented.

Contributing Private Bitcoin to a Business

Private Bitcoin can also be contributed to a business. An increase in value that has already accrued privately is not automatically wiped out for tax purposes. As a rule, the existing acquisition costs are carried forward. If the current value sits below the original acquisition cost, the lower figure can be the relevant one instead. A contribution should therefore be documented with the date, the amount of Bitcoin, the wallet address, the acquisition cost and the market value.

A Clean Split Prevents Bitcoin Tax Problems

Business owners should avoid keeping private and business holdings in the same wallet. Separate wallets, exchange accounts and transaction histories are the sensible route.

What should be documented in particular:

- date of acquisition and purchase price,

- the purpose of the acquisition,

- business deposits and withdrawals,

- wallet transfers,

- contributions and withdrawals,

- fees and sale proceeds.

Conclusion: What Decides Whether Bitcoin Are Business Assets

Whether Bitcoin belong to private or business assets is not decided by the business account alone. What counts is their actual function. Anyone who receives Bitcoin as a customer payment or uses them directly in the business will normally hold them as business assets. A personal investment can remain private property. Particular care is needed with transfers between the company and the private individual, and with Bitcoin held by a limited company. An unclear or retrospectively altered allocation can create additional tax and documentation problems.

(As of August 11, 2026. This article is not investment advice. Prices and fee structures change; check the terms with the provider before you buy.)

Transparency note: This article was produced with the assistance of artificial intelligence and reviewed by our editorial team before publication. All figures and claims were checked against the primary sources linked in the text. The feature image was generated with AI.

Selling Bitcoin at an ATM: the tax duties Austrian users need to know

Bitcoin ATMs are usually associated with a quick and simple crypto purchase. Some machines, however, work in both directions: you can send bitcoin from your wallet to the operator and receive banknotes in return. In tax terms, that transaction amounts to more than a withdrawal from your own digital assets.

Anyone who sells bitcoin for euros at a machine in Austria generally realises a taxable event. For bitcoin acquired after February 28, 2021, the gain can be taxed at 27.5 percent. The taxable figure is the difference between the sale proceeds and the tax acquisition costs of the coins sold, rather than the full cash amount handed over.

Whether the ATM operator already withholds capital gains tax depends on its tax status and on how the transaction is settled. Where no correct withholding takes place, you generally have to work out the gain yourself and report it in your Austrian income tax return. A cash payout makes a bitcoin sale neither anonymous nor tax free.

How selling Bitcoin at an ATM works

At a so called two-way machine you can buy bitcoin as well as sell it. The machine usually displays a receiving address or a QR code. You send the bitcoin you want to sell from your wallet to that address and receive cash once the required number of blockchain confirmations has been reached.

The Austrian financial market authority explicitly describes two-way machines as devices through which bitcoin can be sold from the customer wallet to the operator, with cash paid out in exchange.

In economic terms, two connected steps take place:

- You transfer bitcoin to the ATM operator.

- The operator pays you euros in cash.

For Austrian income tax purposes this is generally a sale of cryptocurrency for euros. It makes no difference whether the proceeds are transferred to a bank account or handed over immediately in banknotes.

Selling Bitcoin for cash is a taxable disposal

The Austrian Income Tax Act explicitly counts the disposal of cryptocurrencies for euros among income from realised capital gains. An exchange for recognised foreign currencies or for other goods and services can also constitute a taxable disposal.

When you sell at a bitcoin ATM, part of your bitcoin holdings leaves your assets and euros come in. That distinguishes the transaction from a simple transfer between two wallets you own yourself.

Transfer between your own wallets: generally not a sale

Transfer to a machine in exchange for cash: generally a taxable sale

The tax treatment does not change because no conventional exchange account is involved. What counts is the economic substance: bitcoin is disposed of in exchange for legal tender.

Only the gain is subject to tax

Tax is not levied on the entire amount paid out at the machine. As a rule, only the gain is taxed.

The simplified calculation is:

Sale proceeds

minus the acquisition costs of the bitcoin sold

minus any deductible transaction costs

equals the taxable gain

An example:

- bitcoin originally bought for 4,000 euros

- later sold at a machine for 7,000 euros

- taxable gain before further costs: 3,000 euros

- tax at 27.5 percent: 825 euros

The 4,000 euros originally invested are not taxed a second time. They represent the tax acquisition costs.

The Austrian finance ministry confirms that the disposal gain is calculated from the difference between the proceeds and the acquisition costs. Directly attributable incidental acquisition and transaction costs can reduce the taxable gain where the statutory conditions are met.

Which amount counts as the sale proceeds?

At a machine, the economic consideration can differ from the publicly quoted bitcoin market price. Operators frequently apply their own exchange rate and factor their margin or fee into the payout.

If you sell bitcoin with an exchange value of 1,000 euros and receive only 920 euros at the machine, the amount actually obtained is generally decisive for the gain calculation. Whether the difference is treated as a separately deductible fee or as part of the agreed sale price depends on how the operator settles the transaction.

The receipt should therefore show:

- how much bitcoin was sold,

- which euro rate was applied,

- which gross value formed the basis,

- which fee or margin was charged,

- which amount was actually paid out.

Without a detailed statement it may later be unclear which part of the difference stemmed from the exchange rate and which from a separate transaction fee.

Which Bitcoin purchase price applies?

If you bought bitcoin in several tranches at different prices, you cannot simply pick the purchase price of any transaction you like.

For units of the same cryptocurrency acquired one after another and held at the same crypto address or wallet, Austria generally requires the moving average price in euros. This valuation method applies to income from realised capital gains received after December 31, 2022.

An example:

- purchase of 0.05 BTC for 1,000 euros

- later purchase of 0.05 BTC for 2,000 euros

- total holding: 0.1 BTC

- total acquisition costs: 3,000 euros

- average acquisition costs: 30,000 euros per BTC

If you then sell 0.02 BTC at a machine, the calculated acquisition costs of that portion generally come to 600 euros. With several wallets, exchange accounts and a mix of legacy and new holdings, the calculation can become considerably more complex. The machine does not know that history automatically.

When does the 27.5 percent rate apply?

The current Austrian crypto tax regime generally applies to bitcoin acquired after February 28, 2021. Such coins are treated as new holdings.

Gains from selling them within private assets are generally subject to the special tax rate of 27.5 percent. The holding period does not change that. A bitcoin held for three, five or ten years does not become tax free on account of that holding period alone.

The special rate normally does not push up the progressive tax rate applied to your remaining income. It applies whether the tax is withheld directly as capital gains tax or assessed later through the income tax return.

A different treatment can apply above all where crypto trading goes beyond private asset management and qualifies as a commercial activity.

What applies to legacy Bitcoin holdings?

Bitcoin acquired on or before February 28, 2021 generally counts as a legacy holding. The new tax regime does not automatically apply to it. The earlier legal position has to be examined instead.

For bitcoin held privately and not invested in an interest bearing way, a sale could be tax free under the old rules, in particular where more than one year lay between acquisition and disposal.

An example:

- bitcoin bought privately in 2019

- no interest bearing investment

- sale at a machine in 2026

In a typical case the former one year speculation period may have expired long ago. The sale could therefore remain tax free. The precise assessment depends on how the coins were used at the time.

Particular care is needed where legacy holdings were later:

- lent out,

- used in lending products,

- invested in an interest bearing way,

- swapped for other tokens,

part of a business activity.

You also have to be able to prove that the coins sold really were those old bitcoin. Merely asserting that a holding is legacy stock is regularly not enough where the transaction history is missing.

Does the machine withhold capital gains tax automatically?

Since 2024, certain domestic debtors and crypto service providers have generally been obliged to withhold capital gains tax on relevant crypto income and pay it to the tax office. After a correct withholding, the income concerned is regularly final taxed within private assets.

At a bitcoin ATM you should nevertheless not assume that the tax has already been settled. Among the decisive points are:

- who operates the machine,

- whether the operator qualifies as a domestic withholding agent,

- whether the statutory conditions for the withholding are met,

- whether the operator holds the correct acquisition costs,

whether the receipt actually shows a tax deduction.

A machine receipt showing a general service fee is no evidence of capital gains tax paid. Withheld tax would have to be clearly identifiable as a tax deduction.

Where no capital gains tax was withheld, the tax liability does not disappear. You generally have to calculate the gain yourself and enter it in your income tax return. The finance ministry makes clear that capital income without a possible domestic tax deduction has to be declared in the assessment. The special tax rate can still apply.

Missing acquisition costs are the biggest practical risk

The operator essentially sees how much bitcoin you send and which euro amount you receive for it. It does not necessarily know:

- when the coins were originally bought,

- how high the purchase price was,

- whether they come from an earlier crypto to crypto swap,

- whether they are legacy or new holdings,

- whether the wallet contains several acquisition tranches,

- whether the coins were inherited or received as a gift,

whether a relocation value is decisive.

Without acquisition costs the gain cannot be determined correctly.

You should therefore not wait until the sale to reconstruct your history. Closed exchange accounts, missing CSV files and bank statements that are no longer available can cause serious problems years later.

The records to secure include:

- purchase statements from the original exchange,

- account statements showing payment of the purchase price,

- complete transaction histories,

- wallet addresses and transaction IDs,

- evidence of transfers between your own wallets,

- information on earlier crypto to crypto swaps,

- documents relating to inheritances or gifts,

documentation of your tax relocation to Austria.

Which fees apply when you sell at a Bitcoin ATM?

Several costs can arise on a sale:

- the machine fee charged by the operator,

- the margin built into the exchange rate,

- the bitcoin network fee,

- an additional processing or payout fee.

These fees should be looked at separately.

A machine or transaction fee directly connected with the sale can generally reduce the taxable disposal gain, provided you actually bear it and can document it in a comprehensible way. The finance ministry generally recognises directly attributable transaction fees when the gain is determined.

The bitcoin network fee can carry a tax component of its own. Where it is paid in bitcoin, coins are used that leave the investor assets. The Austrian income tax guidelines generally treat fees paid in cryptocurrency for a transfer to another address as an exchange for a transaction service.

A machine sale can therefore bring two realisations together:

- the sale of the bitcoin transferred to the operator for euros

- the use of further bitcoin to pay the network fee

In practice the second amount is often small, yet it belongs in a complete tax calculation.

A simplified worked example

An Austrian investor sells 0.02 BTC at a machine.

- average acquisition costs: 20,000 euros per BTC

- acquisition costs of the 0.02 BTC: 400 euros

- market value at the general exchange rate: 1,200 euros

- actual cash payout: 1,100 euros

- separately stated machine fee: already reflected in the payout

- additional network fee: 0.00005 BTC

For the sale itself the simplified result is:

Cash proceeds: 1,100 euros